Learn how to pay quarterly estimated taxes as a freelancer, including deadlines, safe harbor calculations, and how to avoid IRS penalties.

Quarterly Estimated Taxes for Freelancers: A Step-by-Step Guide

If you freelance full-time or earn significant side income, the IRS expects you to pay taxes four times a year, not once at filing time. Understanding how to pay quarterly estimated taxes as a freelancer is one of the most important financial habits you can build. Miss a payment, and you could owe a penalty on top of your actual tax bill.

Key Takeaways

- Freelancers who expect to owe at least $1,000 in federal taxes for the year are generally required to make quarterly estimated payments.

- The IRS charges an underpayment penalty currently calculated at the federal short-term rate plus 3 percentage points, which was 8% as of early 2024.

- The four quarterly deadlines in 2024 fall on April 15, June 17, September 16, and January 15, 2025.

- The safe harbor method lets you base payments on last year's tax liability, which eliminates the underpayment penalty even if you earn significantly more this year.

- Self-employed freelancers pay a self-employment (SE) tax rate of 15.3% on net earnings, which covers Social Security and Medicare, on top of federal income tax.

Who Has to Pay Quarterly Estimated Taxes

The IRS requires quarterly estimated tax payments from anyone who expects to owe $1,000 or more in federal taxes after subtracting withholding and refundable credits. For most freelancers, that threshold is easy to cross.

When you work as an employee, your employer withholds federal income tax and splits the Social Security and Medicare tax burden with you. As a freelancer, no one withholds anything. You are responsible for the entire bill, including the full 15.3% self-employment tax on your net self-employment income up to $168,600 (for 2024), plus the standard federal income tax rate that applies to your bracket.

To put this in context: if you earn $60,000 net as a freelance graphic designer, you could owe roughly $8,478 in self-employment tax alone, before federal income tax is even calculated. Spreading that liability across four payments is not just advisable. It is often legally required.

What Happens If You Skip Payments

The IRS does not wait until April to penalize you. Underpayment penalties are calculated quarterly, meaning each missed or short payment adds to your total. The penalty rate is tied to the federal short-term interest rate and is currently 8% annualized. On a $5,000 underpayment over nine months, that works out to roughly $300 in avoidable fees.

The Four Quarterly Tax Deadlines for 2024 and 2025

The term "quarterly" is slightly misleading because the periods are not evenly spaced. Here are the exact deadlines:

| Payment Period | Due Date |

|---|---|

| January 1 to March 31 | April 15, 2024 |

| April 1 to May 31 | June 17, 2024 |

| June 1 to August 31 | September 16, 2024 |

| September 1 to December 31 | January 15, 2025 |

The second quarter only covers two months of income, which trips up a lot of new freelancers who assume each quarter covers three months equally. If you earn a large contract in April or May, that income still falls into the second quarterly window, and the payment is due by June 17.

If a deadline falls on a weekend or federal holiday, the due date moves to the next business day. Mark these in your calendar now and set a two-week reminder before each one.

How to Calculate How Much to Pay: Two Methods

This is where most freelancers get stuck. The IRS gives you two legitimate approaches for calculating each quarterly payment.

Method 1: The Safe Harbor Method

The safe harbor method is the more predictable of the two. It lets you base your estimated payments on your prior year's tax liability rather than trying to project your current income.

Here is how it works:

- If your adjusted gross income (AGI) in the prior year was $150,000 or less, pay at least 100% of last year's total tax liability spread across four equal payments.

- If your prior year AGI exceeded $150,000, pay at least 110% of last year's total tax liability.

As long as you meet that threshold, the IRS cannot charge you an underpayment penalty, even if you earn twice as much this year and ultimately owe significantly more in April.

Example: Suppose freelance copywriter Marcus Webb earned $75,000 net in 2023 and paid $14,200 in total federal taxes. His safe harbor target for 2024 is 100% of that amount, which means he needs to send the IRS $3,550 per quarter. If Marcus lands a major retainer in 2024 and earns $110,000, he will owe additional taxes in April 2025. But he will not owe any underpayment penalty, because he satisfied the safe harbor threshold.

This method works best for freelancers with relatively stable income or those who had a particularly high-earning prior year.

Method 2: The Actual Income Method (Annualized Income Installment Method)

This approach requires you to estimate your current year income as accurately as possible each quarter and pay tax based on that projection.

The IRS provides Form 2210 and its worksheet specifically for freelancers who want to use actual income estimates. The calculation involves:

- Estimating your net self-employment income for the quarter.

- Calculating the 15.3% self-employment tax on that income.

- Deducting the 50% employer-equivalent SE tax deduction (which reduces your AGI).

- Applying your federal income tax bracket to the remaining income.

- Totaling both liabilities and paying that amount by the deadline.

Example continued: If Marcus had a slow first quarter in 2024 and earned only $12,000 net, using the actual income method he might only owe around $2,700 for that period. That is $850 less than the safe harbor payment. The actual income method preserves cash flow in lean quarters but requires more math and better recordkeeping.

Which Method Should You Choose

The safe harbor method is safer and simpler, as the name implies. The actual income method can reduce your payments in a slow year, but it requires you to track income carefully and recalculate each quarter. Most freelancers who earn above $75,000 per year use safe harbor to stay penalty-free and then reconcile any remaining balance in April.

How to Pay Quarterly Estimated Taxes as a Freelancer

Knowing the amount is only half the equation. Here is exactly how to submit your payments to the IRS.

Step 1: Set Up an IRS Direct Pay Account

The fastest and most reliable method is IRS Direct Pay at irs.gov/payments. You can pay directly from your checking or savings account with no fees. Payments can be scheduled up to 30 days in advance, which makes it easy to automate your quarterly reminders.

Step 2: Use the Electronic Federal Tax Payment System (EFTPS)

EFTPS (eftps.gov) is the IRS's full payment system for individuals and businesses. It requires a one-time enrollment but allows you to schedule all four quarterly payments at the start of the year. For freelancers managing cash flow carefully, scheduling payments in advance eliminates the risk of forgetting a deadline.

Step 3: Mail a Check With Form 1040-ES

If you prefer a paper trail, you can mail a check payable to "United States Treasury" along with the corresponding 1040-ES payment voucher for that quarter. Mail it early enough to arrive by the due date. The IRS uses the postmark date, not the date received, but it is safer not to cut it close.

Step 4: Keep Records of Every Payment

Save confirmation numbers from every Direct Pay or EFTPS transaction. If the IRS ever questions whether you made a payment on time, a confirmation number or a canceled check is your proof. Store these alongside your quarterly income records.

How to Pay Quarterly Estimated Taxes as a Freelancer: Practical Tips for Staying on Track

Setting aside money throughout the year is just as important as knowing when to pay.

Most tax professionals recommend that self-employed freelancers set aside 25% to 30% of every payment they receive into a dedicated savings account. If you are in the 22% federal bracket and add the 15.3% SE tax (reduced by the deductible portion to about 14%), you are looking at a combined effective rate close to 30% on net income.

Opening a separate high-yield savings account labeled "Tax Reserve" creates a psychological and practical barrier between your operating cash and your tax liability. Transfer a fixed percentage immediately when a client payment lands.

Save Time on the Math With the Right Tool

If the calculations above felt like a lot to track manually, that is because they are. Estimating net income, applying the SE tax, running the safe harbor comparison, and staying organized across four quarters takes real time.

The Freelancer Quarterly Tax Estimator template was built to do exactly this work for you. It walks you through each quarter, calculates your safe harbor target and your actual income estimate side by side, and tells you precisely what to send the IRS by each deadline. It is available for $14 at tdniverse3.gumroad.com/l/tjbqdo and takes about 15 minutes to complete per quarter.

If this post saved you from an underpayment penalty, the template can save you from doing this math again from scratch every 90 days.

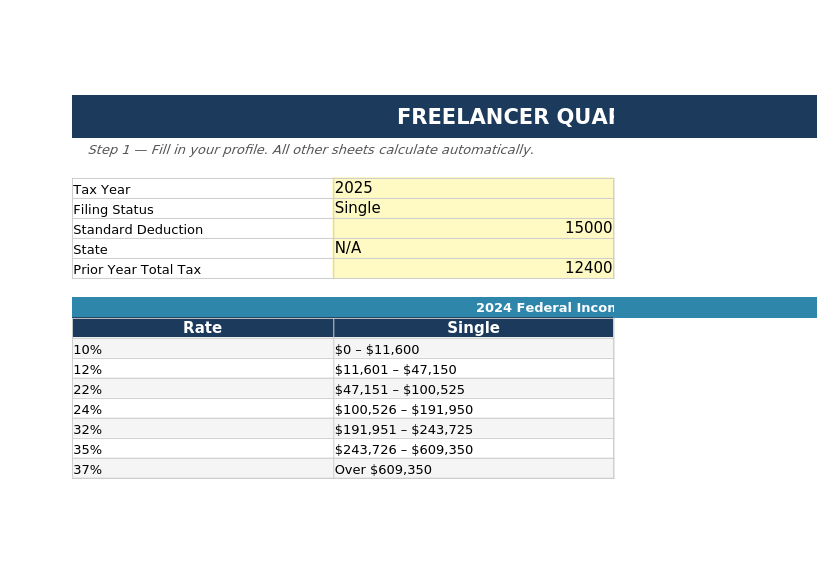

What the Template Looks Like

Here is a preview of the Freelancer Quarterly Tax Estimator with sample data filled in:

The Bottom Line

Quarterly estimated taxes are not optional for most freelancers, and the IRS charges real penalties for missing or underpaying them. Using the safe harbor method is the most reliable way to stay penalty-free while keeping your calculations manageable. Set aside 25% to 30% of every payment, mark the four deadlines in your calendar, and use IRS Direct Pay to submit on time.