Learn how to create a business budget that actually works, with a step-by-step process, budget vs. actual tracking tips, and fixes for the most common mistakes.

How to Create a Business Budget That You Will Actually Stick To

Learning how to create a business budget is straightforward. Getting yourself to follow it for more than two months is the hard part. Most small business owners build a budget once, file it away, and return to making financial decisions from gut feel. This guide covers the full process of building a budget that works in practice, including the one tracking habit that separates businesses that hit their targets from those that constantly wonder where the money went.

Key Takeaways

- Small businesses that review a formal budget monthly are 20% more likely to be profitable than those that do not, according to a U.S. Bank study on cash flow management.

- A functional business budget tracks five core categories: revenue, cost of goods sold, fixed expenses, variable expenses, and owner compensation.

- The average small business owner underestimates annual operating expenses by 15% to 25%, largely due to ignoring irregular costs like insurance renewals and equipment repairs.

- Budget vs. actual tracking, comparing what you planned to what you actually spent, is the single most effective habit for keeping a budget alive month after month.

- A business with $300,000 in annual revenue should expect to spend 30 to 60 minutes per month on budget review to maintain meaningful financial oversight.

Why Most Business Budgets Fail Before March

The most common reason a business budget fails is not poor math. It is that the budget gets built in January and never opened again.

A budget without a review process is just a spreadsheet. It captures your best guess about the future but does nothing to correct course when reality diverges from that guess. And it will diverge. Raw material costs increase, a slow month hits harder than expected, or a new hire pushes payroll beyond projections.

The fix is not a better spreadsheet template. It is a consistent review habit built directly into your monthly routine.

How to Create a Business Budget: A Step-by-Step Process

Step 1: Establish Your Revenue Baseline

Start with what you actually earned, not what you hope to earn. Pull your total gross revenue for the past 12 months. If your business is newer than a year, use every month of data you have.

Break revenue down by product line, service type, or customer segment if possible. A landscaping company, for example, might separate residential mowing contracts from one-time hardscape projects, because those revenue streams have very different profit margins and seasonality patterns.

Once you have your historical numbers, apply a conservative growth rate for the year ahead. For most small businesses, 5% to 15% is realistic. Overestimating revenue is the most dangerous mistake in budgeting because it inflates every spending decision that follows.

Step 2: Categorize Every Expense

Expenses fall into four buckets that every business budget needs to treat separately.

Cost of Goods Sold (COGS): These are the direct costs tied to delivering your product or service. For a bakery, COGS includes flour, butter, and packaging. For a marketing consultant, it includes contractor fees paid to support a specific client project.

Fixed Expenses: These stay the same regardless of revenue. Rent, software subscriptions, loan payments, and base salaries are fixed. A business paying $2,400 per month in rent pays $28,800 per year in fixed overhead whether it earns $150,000 or $400,000.

Variable Expenses: These scale with business activity. Shipping costs, sales commissions, and credit card processing fees are variable. When revenue rises, these rise too. When revenue drops, they should fall.

Irregular Expenses: This is the category most budgets skip entirely, and it is why so many businesses feel blindsided by cash crunches. Annual insurance premiums, quarterly estimated taxes, equipment servicing, and professional development costs are real and predictable. Divide each annual cost by 12 and include it as a monthly line item.

Step 3: Calculate Your Gross and Net Profit Targets

Once you have revenue and expenses mapped out, calculate your projected gross profit margin and net profit margin.

Gross profit margin is revenue minus COGS, divided by revenue. For a product-based business, a healthy gross margin typically runs between 40% and 60%. For service businesses, it often runs higher, sometimes 70% or more, because labor replaces physical inventory.

Net profit margin is what remains after all expenses, including owner compensation. Many small business owners skip paying themselves a formal salary, which makes their profit look stronger than it actually is. Budget for owner compensation as a line item before calculating net profit. A reasonable target for an established small business is 10% to 20% net profit margin.

Step 4: Build Your Monthly Budget Template

A practical business budget breaks the year into 12 monthly columns. For each month, you need three fields per line item: budgeted amount, actual amount, and variance.

This three-column structure is what transforms a budget from a wish list into a management tool. The variance column, which shows the difference between what you planned and what happened, tells you exactly where to focus your attention each month.

You do not need expensive software to do this. A well-structured spreadsheet handles most of what a small business needs up to about $2 million in annual revenue.

A Real Example: How Marcus Built a Budget That Held

Marcus Delgado owns a residential cleaning company in Phoenix called Sunrise Home Services. In 2022, he was bringing in roughly $180,000 per year but consistently felt cash-strapped. He knew his revenue but had no clear picture of where it was going.

He sat down in December and built his first real budget for 2023. He categorized $54,000 in COGS (cleaning supplies, contract labor), $42,000 in fixed expenses (insurance, van lease, software), and $18,000 in variable expenses (fuel, replacement equipment). He set an owner salary of $52,000, leaving a projected net profit of $14,000, or about 7.8%.

When March arrived, Marcus compared his actuals to his budget and found that fuel costs had run $600 over projections in just two months. That variance triggered a review: he had not accounted for rising gas prices when building the variable expense line. He adjusted his April through December fuel budget upward by $250 per month. The result was a budget that stayed relevant for the full year instead of becoming useless by spring.

By December 2023, Marcus finished the year with an actual net profit of $12,400, close to his $14,000 projection. More importantly, he had avoided three cash flow crunches that would have blindsided him without the monthly tracking habit.

The Budget vs. Actual Review: How to Do It Monthly

Set a recurring calendar block on the same day each month, ideally within the first five business days after the month closes. The review itself should take 30 to 60 minutes.

What to Check in Your Monthly Review

Work through each major category in order: revenue first, then COGS, then fixed expenses, then variable expenses. For any line item where the variance exceeds 10%, ask two questions: Is this a one-time event or a recurring pattern? Does the budget need to be adjusted for future months?

A one-time variance, like an unexpected equipment repair, does not require a budget change. It requires a note. A pattern, like labor costs running over budget three months in a row, signals that the original estimate was wrong and needs correction.

This is the mechanism that keeps a budget alive. Most people skip it. The ones who do not are the ones whose budgets actually work.

When to Revise Your Budget Mid-Year

A budget is not a legal contract. Revise it when material changes occur: a significant new client, a major expense reduction, or a shift in your service mix. Businesses typically revise their annual budget one or two times per year. Revising more than quarterly usually means the original budget was built too quickly.

Common Budgeting Mistakes to Avoid

Ignoring owner compensation: If you do not pay yourself a salary in the budget, the numbers are not accurate. Period.

Using last year's revenue as a ceiling: Historical performance is a baseline, not a limit. Apply a growth assumption, even a modest one.

Forgetting tax liability: Set aside 25% to 30% of net profit each month for estimated taxes. This prevents the annual scramble that catches many self-employed business owners off guard.

Building only an annual total: Monthly breakdowns matter because cash flow is monthly. A business might be profitable annually but cash-negative in February if it does not plan for seasonality.

A Tool That Does the Work for You

If you want to put this process into practice without building a spreadsheet from scratch, the Business Budget Planner template at smallbizfinancehq.com/templates is structured exactly around the method described in this guide. It includes the 12-month layout, pre-built categories for COGS and variable expenses, a budget vs. actual variance tracker, and a net profit summary tab. At $12, it is built for small business owners who want a clean, working tool without the setup time. It handles the structure so you can focus on the numbers.

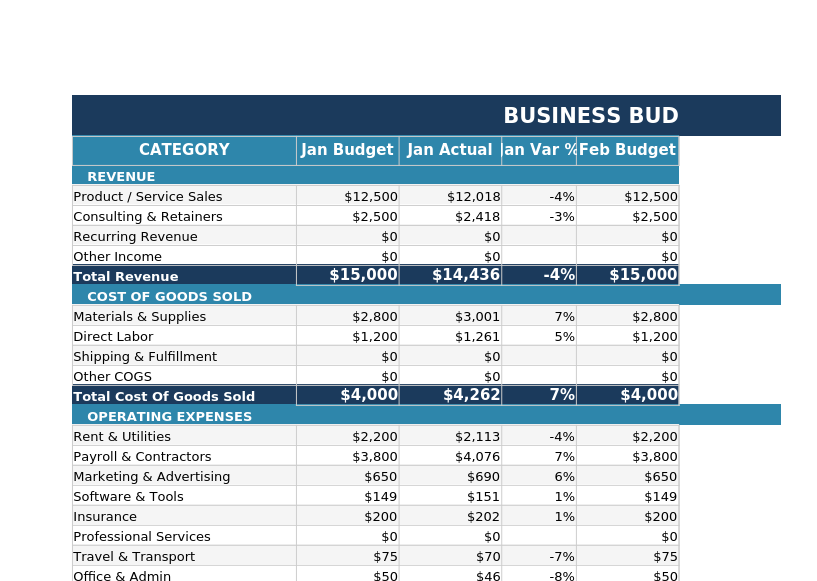

What the Template Looks Like

Here is a preview of the Business Budget Planner with sample data filled in:

The Bottom Line

A business budget works when it gets reviewed, adjusted, and taken seriously as a management tool, not treated as a one-time planning exercise. The most important step in this entire process is not building the budget, it is committing to the monthly comparison between what you planned and what actually happened. For most small businesses, that habit alone will surface thousands of dollars in untracked spending and missed opportunities within the first year.