Learn how to build a 12-month cash flow forecast for your small business, avoid cash shortfalls, and plan for seasonal swings and growth with confidence.

How to Build a Cash Flow Forecast for Your Small Business

A cash flow forecast for your small business is not a luxury reserved for companies with a full-time CFO. It is the single most practical financial tool a small business owner can use to stay solvent, plan for growth, and stop making decisions in the dark. Done right, a 12-month forecast tells you exactly when money will be tight, when you can afford to hire, and when you need a line of credit before the bank asks why you need one.

Key Takeaways

- Small businesses with a formal cash flow forecast are 30% more likely to survive their first five years, according to U.S. Bank research on business failure causes.

- A 12-month rolling forecast requires as few as five core inputs: beginning cash balance, projected revenue, cost of goods sold, fixed operating expenses, and variable expenses.

- Seasonal businesses should build two forecast scenarios, a peak-season version and an off-season version, to avoid drawing down reserves at the wrong time.

- A cash shortfall identified 60 to 90 days in advance gives you negotiating power with lenders. A shortfall identified on the day payroll is due gives you a crisis.

- The difference between a cash flow forecast and a profit and loss statement is timing. Revenue recorded in April may not land in your bank account until June.

Why Forecasting Beats Reacting

Most small business owners manage cash the same way: check the bank balance each morning, pay what is urgent, and hope the rest works out. That approach fails quietly until it fails catastrophically.

Forecasting shifts you from reactive to proactive. Instead of discovering a shortfall when vendors are calling, you see it 90 days ahead and have time to adjust. You can delay a capital purchase, push a hire back one quarter, or secure a credit line while your financials still look healthy.

Here is why that matters in practical terms. Lenders evaluate creditworthiness on recent history. If you apply for a loan during a cash crunch, your statements reflect the crisis. If you apply three months before the crunch, using forecast data to demonstrate you understand your own business cycle, you are a far more attractive borrower.

What a Cash Flow Forecast Actually Includes

A cash flow forecast is not the same as a budget. A budget reflects what you plan to spend. A forecast reflects when cash will actually move in and out of your account.

The Five Core Components

Every solid small business cash flow forecast is built on five inputs.

1. Beginning Cash Balance This is your starting point for each month. Whatever cash sits in your operating account on the first of the month is your opening number. Do not include credit lines you have not drawn on.

2. Cash Inflows This covers all money entering your account: customer payments, loan proceeds, owner contributions, and any other income. For product businesses, this is when customers pay, not when you invoice them. A net-30 invoice sent on March 1 becomes a cash inflow in April.

3. Cost of Goods Sold (COGS) If you sell physical products or deliver billable services, your COGS moves with revenue. A landscaping company that earns $40,000 in June might spend $18,000 on labor and materials to generate that revenue. Both numbers belong in the June column.

4. Fixed Operating Expenses Rent, insurance, software subscriptions, loan payments, and base salaries are fixed costs that hit every single month regardless of revenue. These are the easiest to forecast because they rarely change.

5. Variable Operating Expenses Marketing spend, contractor fees, utilities, and shipping costs fluctuate. Use a three-month average from your actual books to estimate these, then adjust for known changes like a planned ad campaign or a seasonal staffing increase.

How to Build Your 12-Month Cash Flow Forecast

Building the forecast takes an afternoon the first time. Once the structure is in place, updating it takes about 20 minutes per month.

Step 1: Pull Three to Six Months of Actual Data

Start with your bank statements and accounting software. You want real revenue by month, real expenses by category, and your actual beginning cash balance for the most recent month. This data becomes the foundation for your assumptions.

Step 2: Set Your Revenue Assumptions

Project revenue month by month using one of two methods. If your business is steady, apply a conservative growth rate, typically 3% to 8% per month depending on your industry and stage. If your business is seasonal, use last year's monthly revenue as your baseline and adjust for any known changes, a new product line, a price increase, a lost client.

Do not project revenue from best-case scenarios. Project from your most likely scenario. You can build a separate optimistic version, but your primary forecast should be conservative enough that you can actually meet it.

Step 3: Map Your Expenses by Month

List every fixed expense and assign it to the correct month. Then layer in variable expenses using your historical averages. Flag any months where you expect one-time costs: equipment purchases, trade show fees, tax payments, or annual insurance renewals.

This step is where most business owners undercount. Quarterly expenses get forgotten. Annual software renewals go unbudgeted. Build a running list of every non-monthly expense you paid last year and distribute them into the correct months.

Step 4: Calculate the Net Cash Position

For each month, subtract total outflows from total inflows and add that number to your beginning cash balance. The result is your ending cash balance, which becomes next month's beginning balance. A negative ending balance in any month signals a cash shortfall that needs a plan.

Step 5: Add a Minimum Cash Buffer

Determine the minimum cash balance you need to feel operationally safe. For most small businesses, this is one to two months of fixed operating expenses. If your fixed costs run $15,000 per month, your minimum buffer is $15,000 to $30,000. Any forecasted month that drops below that threshold deserves attention before it arrives.

Cash Flow Forecasting for Seasonal Businesses

Seasonal businesses face a specific challenge: revenue is lumpy, but expenses are not. A retail gift shop in Vermont might generate 60% of its annual revenue between November and January. Rent still comes due in July.

A Real Example: Coastal Coffee Roasters

Consider Coastal Coffee Roasters, a small-batch roasting company based in Charleston, South Carolina. Their wholesale accounts are steady year-round, generating about $12,000 per month. But their direct-to-consumer online sales spike hard in November and December, adding $28,000 to $35,000 per month during the holiday season.

The owner, Marcus, made a common mistake in his first three years. He spent aggressively in January and February, flush with holiday cash, then found himself short on operating capital by April when wholesale receivables ran slow and online sales had dropped back to $6,000 per month.

In year four, Marcus built a 12-month cash flow forecast with two revenue tracks: his stable wholesale line and his variable DTC channel. The forecast showed him clearly that his April-to-June period was chronically underfunded. He adjusted by holding $22,000 in reserve after the holiday season and pre-paying three months of his roasting facility lease in December when cash was flush. His next spring was the first in four years he did not have to put personal expenses on a credit card.

The lesson is straightforward. A seasonal forecast does not just tell you when money arrives. It tells you how to manage the timing gap between your flush months and your lean ones.

Using Your Forecast for Growth Planning

A cash flow forecast is not only a defensive tool. It is how smart owners evaluate whether they can actually afford to grow.

When to Hire, When to Wait

Hiring a full-time employee at $55,000 per year costs roughly $63,000 to $67,000 when you include payroll taxes and benefits. Before you post the job listing, your forecast should show 12 months of positive cash flow after that expense is added. If it does not, you are not ready to hire full-time. You may still be ready to hire a part-time contractor at $2,000 per month, which is a very different cash commitment.

Evaluating a New Revenue Line

If you are adding a new product or service, build a conservative revenue ramp into the forecast. Most new offerings take three to six months to reach meaningful revenue. Your forecast should reflect that startup period honestly, including any upfront costs for inventory, marketing, or equipment.

Build Your Forecast Without Starting From Scratch

If you have read this far, you understand the logic. The harder part is setting up a clean spreadsheet that handles the formulas, tracks the monthly rollover, and organizes all five components in a format you will actually use.

The Cash Flow Projection template at smallbizfinancehq.com/templates is built for exactly this process. For $15, you get a pre-formatted 12-month Excel spreadsheet that includes separate input sections for fixed and variable expenses, an automatic beginning-to-ending balance rollover, and a visual summary that flags shortfall months in red. It puts into practice everything covered in this post so you spend your afternoon analyzing your numbers, not formatting cells.

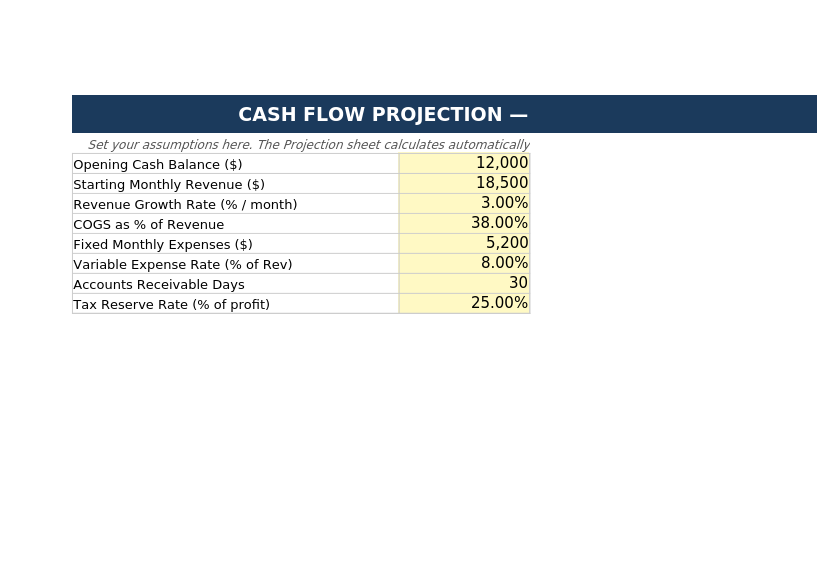

What the Template Looks Like

Here is a preview of the Cash Flow Projection with sample data filled in:

The Bottom Line

A cash flow forecast for your small business is the difference between managing your finances and guessing at them. The mechanics are straightforward: track when cash comes in, track when it goes out, and identify the gaps before they become emergencies. Seasonal businesses, growth-stage companies, and steady-state operations all benefit from the same discipline. Build the forecast once, update it monthly, and it will pay for itself the first time it shows you a problem three months before it arrives.